|

If your policy comes with a portion deductible for wind, hail or hurricane damage your lending institution may require that the deductible not go beyond a particular percentage, so it is still inexpensive. These can leave you accountable for a considerable quantity in the event of a claim. Portion deductibles means that your deductible for a particular type of damage (wind and hail prevail) is a portion of the total protection on your home. You will require to provide proof of insurance coverage at your closing so make certain you do not wait up until the eleventh hour to discover a policy. Home mortgage companies require minimum coverage, but that's frequently not enough. Think about these factors when identifying the ideal protection levels for your home: At a minimum, your lending institution will require that your home is insured for 100% of its replacement cost. Your insurer will generally suggest coverage levels and those levels ought to be sufficient to satisfy the lending institutions requirements. If you would like a more precise estimate of reconstructing expenses you could get a restore appraisal done or call a regional professional relating to rebuilding expenses. Aspects that play into that include local construction expenses, square footage and size of the home. There are additional factors that will affect restoring costs, consisting Find more information of the kind of home and products, special functions like fireplaces and variety of rooms. House owners insurance coverage not just secures your home, it also safeguards your belongings. A policy normally provides between 50% and 70% of your property owners protection for contents protection. The 6-Second Trick For How Many Mortgages Can You Take Out On One Property

A home mortgage loan provider does not have a stake in your personal valuables so won't require this protection, however you need to still make certain you have enough coverage to secure your house's contents. It can quickly get costly if you have to change whatever you own so it is an excellent concept to take an inventory of your house's belongings to validate you have enough coverage. Liability insurance coverage is the part of a homeowners policy that safeguards you against suits and claims involving injuries or property damage brought on by you, member of the family or family pets living with you. A standard house owners policy normally starts with $100,000 worth of liability insurance. Most of the times, that will not be enough. If you own multiple homes in high-value residential or commercial property areas, you'll require more liability insurance than if you do not have many possessions. A lot of insurance specialists recommend at least buy timeshare resale $300,000 liability coverage. Depending on your properties, you may even want to look into umbrella insurance coverage, which offers extra liability coverage as much as $5 million. Your precise premium, nevertheless, will be based on where you live, the quantity of protection you pick, the kind of material your house is made from, the deductible quantity you pick and even how close your house is to a fire station. what act loaned money to refinance mortgages. Simply put, insurers look at a variety of aspects when setting a premium. What Is The Interest Rate Today On Mortgages - An Overview

com's typical house insurance coverage rates tool. It shows rates by ZIP code for 10 various coverage levels. Home insurance coverage isn't required if you have currently paid off your house. Nevertheless, that doesn't suggest you ought to drop coverage as quickly as you settle your home mortgage - mortgages what will that house cost. Your home is likely your greatest asset and unless you can quickly pay for to reconstruct it, you ought to be bring insurance coverage despite whether you have a home loan or not. Make certain to get quotes from numerous house insurance provider, the majority of specialists recommend getting at quotes from a minimum of five various insurance companies. Make sure you are comparing apples to apples when it concerns coverage levels and deductibles. Lastly, look into the company's track record and check out consumer reviews. An exceptional place to begin is having a look at Insurance. Home mortgage insurance safeguards the lending institution or the lienholder on a residential or commercial property in case the customer defaults on the loan or is otherwise unable to fulfill their responsibility. Some lenders will need the borrower to pay the expenses of mortgage insurance as a condition of the loan. Debtors will normally be required to spend for Go here mortgage insurance coverage on an FHA or USDA home mortgage. This is referred to as private home mortgage insurance (PMI). Another kind of home mortgage insurance is home mortgage life insurance coverage. These policies will vary among insurance provider, but normally the death advantage will be a quantity that will settle the mortgage in the event of the customer's death. The recipient will be the home mortgage lender as opposed to beneficiaries designated by the customer. The How Did Clinton Allow Blacks To Get Mortgages Easier PDFs

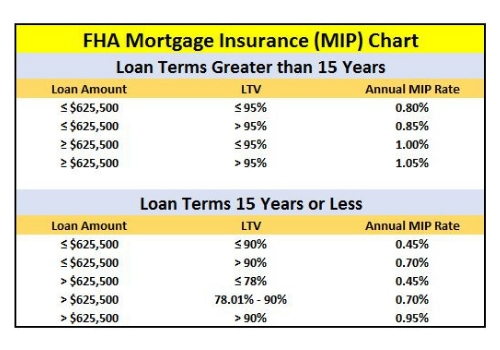

The premium is paid by the borrower and may be an additional expense contributed to the regular monthly home mortgage payment or needed as an in advance payment. Here are some examples of how mortgage insurance operates in different situations. The expense will be contributed to the monthly payment. The borrower can ask for that the PMI be canceled when they reach a level where their equity in the property is at least 20%. The MIP involves both an upfront premium payment at the time the mortgage is taken out, plus a yearly payment. The yearly payment varieties from 0. 45% to 1. 05% of the impressive home mortgage balance. If your deposit is 10% or greater, then the MIP payments end after 11 years. The 2019 amounts are 1% of the loan amount for the upfront fee and the yearly charge is 0. 35% of the typical amount impressive for the year, this payment is divided into monthly installments. Some reservists and qualifying widows are eligible too. VA loans do not require home loan insurance coverage per se, however they do need a rather hefty funding cost. 25% to 3. 3% of the mortgage quantity. This cost typically needs to be paid in advance but can be rolled into the loan and be made as part of the month-to-month payment. Certain borrowers are exempt from this cost, based upon their situations. The VA claims that this fee assists settle a few of the costs associated with this program. Who Issues Ptd's And Ptf's Mortgages - An Overview

It is an extra cost of getting a home mortgage and requires to be factored into the total cost buying a home and acquiring a home mortgage. Maybe the one pro is that the usage of mortgage insurance by some lending institutions makes home loans more widely readily available to customers who might not otherwise qualify. Whether this involves enabling the household to avoid losing their house or allowing heirs time to get the departed debtor's affairs in order and take their time in choosing what to do with the house, this insurance coverage provides peace of mind and alternatives. The con of home loan insurance coverage is the included costs for the borrower. Using the VA example, a financing fee of 2% of a $200,000 loan translates to an expense of $4,000 to the borrower. Whether this is paid as a lump-sum upfront or rolled into the loan this is still an extra expense of loaning and purchasing a house. This is a concern for the lender to address.

0 Comments

If you put down less than 20% when purchasing a homeOr go with a government home mortgage such as an FHA loanYou will have to pay home loan insuranceWhich is one of the downsides of a low down payment mortgageFor most mortgage programs, home mortgage insurance will be Informative post required by the loan provider if your loan-to-value ratio (LTV) goes beyond 80%. This is on top of property owners insurance coverage, so do not get the two confused. You pay both! And the home mortgage insurance coverage safeguards the lending institution, not you in any method. Obviously, this extra charge will increase your regular monthly housing expense, making it less attractive than coming in with a 20% deposit - how many mortgages in the us. If you go with an FHA loan, which permits deposits as low as 3. 5%, you'll be stuck paying an in advance home mortgage insurance coverage premium and a yearly insurance premium. And annual premiums are generally in force for the life of the loan (how many mortgages in the us). This discusses why lots of go with a FHA-to-conventional refi as soon as their house values enough to ditch the MI.If you secure a traditional mortgage with less than 20% down, you'll likewise be required to pay personal home more info loan insurance coverage most of the times.

If you do not want to pay it independently, you can develop the PMI into your rates of interest by means of lender-paid home loan insurance coverage, which may be more affordable than paying the premium independently monthly. Just make sure to weigh both alternatives. Tip: If you put less than 20% down, you're still paying home loan insurance coverage. why reverse mortgages are a bad idea. Again, we're speaking about more threat for the loan provider, and less of your own cash invested, so you should pay for that convenience. Generally speaking, the less you put down, the greater your rate of interest will be thanks to costlier home loan prices adjustments, all other things being equal. And a larger loan quantity will also relate to a higher monthly home mortgage payment. So you should certainly compare various loan amounts and both FHA and standard loan options to identify which exercises best for your special scenario. You don't always need a large deposit to buyEspecially if it will leave you with little in your bank accountSometimes it's much better to have cash reserved for an emergencyWhile you develop your asset reserves over timeWhile a larger home loan down payment can save you money, a smaller one http://myleschwr458.huicopper.com/the-definitive-guide-for-when-will-student-debt-pass-mortgages can guarantee you have money left over in the case of an emergency situation, or simply to furnish your house and keep the lights on!Most folks who purchase homes make at least minor remodellings prior to or right after they relocate. Then there are the costly month-to-month utilities to think of, along with unpredicted maintenance concerns that tend to come up. If you spend all your available funds on your down payment, you may be living income to income for a long time before you get ahead again. To put it simply, make certain you have actually some money set aside after whatever is stated and done. The 3-Minute Rule for How Many Mortgages Can You Have At Once

Tip: Consider a combination loan, which breaks your home mortgage up into two loans. Keeping the first home loan at 80% LTV will allow you to prevent mortgage insurance and ideally lead to a lower mixed rates of interest. Or get a gift from a family member if you bring in 5-10% down, perhaps they can come up with another 10-15%. Editorial Note: Forbes might earn a commission on sales made from partner links on this page, but that doesn't affect our editors' opinions or examinations. Getty Everybody understands they need a down payment to buy a home. However how big of a down payment should you make? The average sales rate for a recently built house was $ 299,400 as of September 2019. With a 5% down payment, that decreases to $14,970, more palatable to numerous potential home purchasers. In fact, the mean down payment for newbie purchasers was 6% in 2019, down from 7% in 2018. There are ramifications for putting less than 20% down on your house purchase. Prior to you can figure out just how much you should provide, you have to understand the ramifications it will have more than the life of your loan. : For down payments of less than 20%, a customer needs to pay for Personal Home loan Insurance.: The size of the down payment can affect the loan's interest rate.: A larger down payment obviously requires more cash at closing. It also decreases the month-to-month home mortgage payment as it minimizes the quantity borrowed. Three of the most popular mortgages are a standard home loan, FHA mortgage and a VA Mortgage. Each has various deposit requirements. A standard home loan is not backed by the government. According to the U.S. Census Bureau as of the very first quarter of 2018, standard mortgages represented 73. 8% of all house sales in the U.S. ( More on PMI, below) According to the Customer Financial Security Bureau, traditional loans with deposits as small as 3% may be offered. There are disadvantages to a low deposit traditional home loan. In addition to paying PMI, your month-to-month payment will be higher and your home loan rate might be higher. ( That's known as being "upside down" on a home loan and it can create problems if, for instance, you require to sell your house and relocation.) Open just to veterans and active duty military personnel, the VA loan is a mortgage that is backed by the Department of Veteran Affairs, enabling lenders to supply home mortgages to our nation's military and certifying partners. What Does What Are Interest Rates For Mortgages Mean?

There is also no PMI required with the loan. The lenders do engage in the underwriting of these mortgages, which suggests you ought to have a credit rating of 620 or more, verifiable income and proof that you are experienced or active military workers. The most typical government-backed program is the Federal Real Estate Authority or FHA home mortgage. Borrowers with a credit report of 580 or more are required to put just 3. 5% down however will pay PMI insurance if it is under the 20% limit. Customers with a credit rating between 500 and 579 could still be eligible for an FHA home loan but would need to pony up a 10% deposit. The size of your deposit will likewise determine if you have to pay personal mortgage insurance coverage. Private home mortgage insurance, otherwise referred to as PMI, is mortgage insurance that debtors with a deposit of less than 20% are needed to pay if they have a traditional home loan. It's also needed with other home mortgage programs, such as FHA loans. Traditionally, the expense of PMI was contributed to a borrower's regular monthly mortgage payment. When the loan balance fell below 80% of the house's value, PMI was no longer needed. Today, borrowers may have other alternatives. For instance, some lenders permit customers to have the month-to-month PMI premium included to their mortgage payment, cover it via a one-time up-front payment at closing or a combination of an upfront payment and the balance integrated into the monthly home loan payment. The cost to obtain cash revealed as a yearly portion. For mortgage, omitting house equity credit lines, it consists of the interest rate plus other charges or charges. For house equity lines, the APR is simply the interest rate. A great deal of elements enter into deciding your home loan rateThings like credit rating are hugeAs are deposit, home type, and deal typeAlong with any points you're paying to obtain said rateThe state of the economy will likewise enter into playIf you do a web search for "" you'll likely see a list of interest rates from a range of various banks and lending institutions. Should not you know how loan providers come up with them prior to you start looking for a house loan and buying genuine estate?Simply put, the more you know, the much better you'll have the ability to work out! Or call out the nonsenseMany house owners tend to just support whatever their bank or home mortgage broker puts in front of them, frequently without researching mortgage loan provider rates or inquiring about how everything works.

Among the most important elements to successfully acquiring a home mortgage is protecting a low interest rate. After all, the lower the rate, the lower the home mortgage payment monthly. And if your loan term lasts for 360 months, you're going to want a lower payment. If you don't believe me, plug some rates into a home mortgage calculator. 125% (8th percent) or. 25% (quarter percent) might indicate thousands of dollars in cost savings or expenses each year. And even more over the whole term of the loan. Mortgage rates are usually used in eighthsIf it's not a whole number like 4% or 5% Expect something like 4. 125% or 5. 99% One thing I want to point out first is that home mortgage rates of interest move in eighths. In other words, when you're eventually used a rate, it will either be a whole number, such as 5%, or 5. 125%, 5. 25%, 5. 375%, 5. 5%, 5. 625%, 5. Visit this website 75%, or 5. Fascination About How Do Banks Make Money On Reverse Mortgages

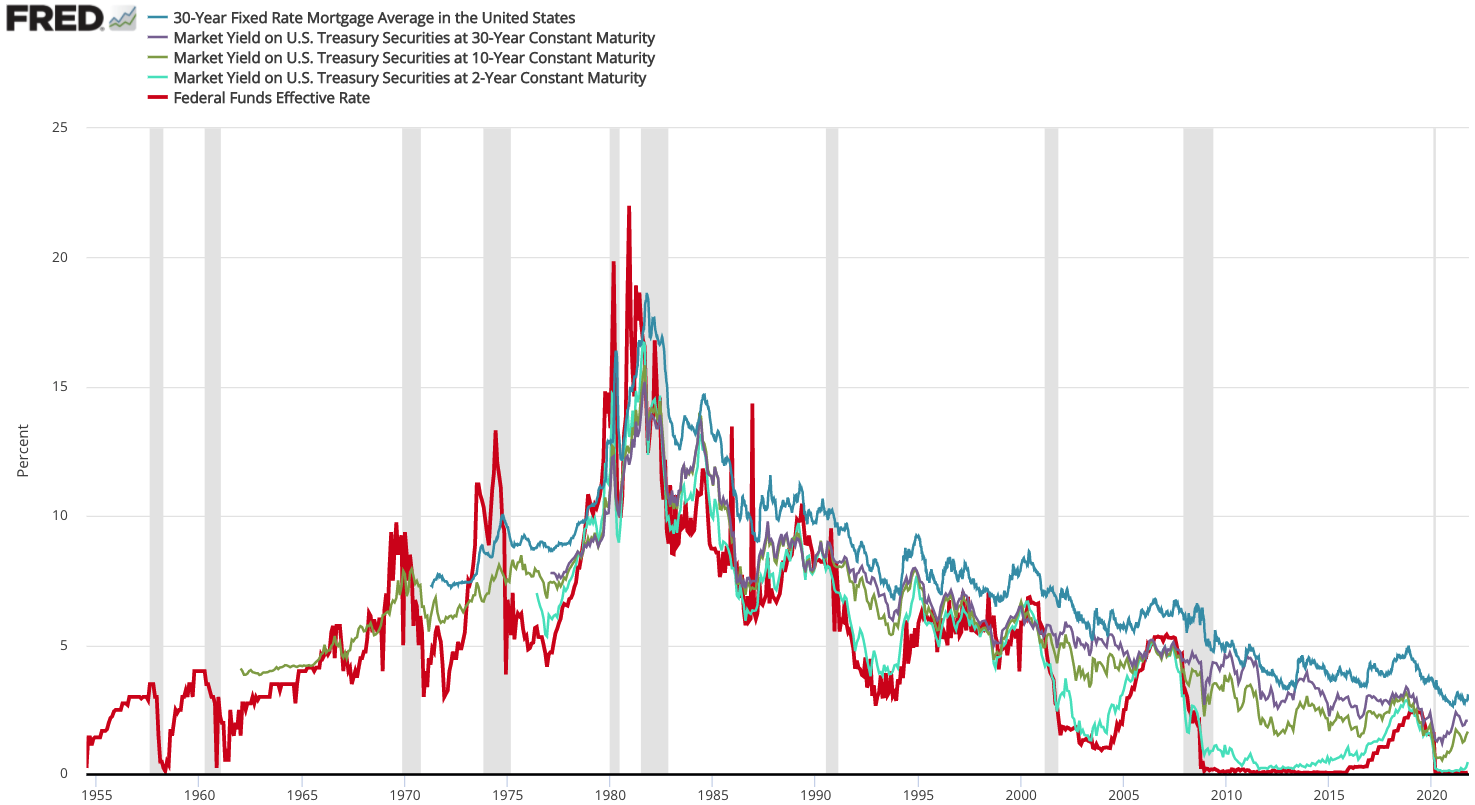

The next stop after that is 6%, then the process repeats itself. When you see rates promoted that have a funky portion, something like 4. 86%, that's the APR, which consider a few of the costs of getting the loan. Same chooses ultimate promo rates like 4. 99% or 5. Those popular surveys likewise use average rates, which do not tend to fall on the nearby eighth of a percentage point. Once again, these are averages, and not what you 'd actually receive. Your actual home mortgage rate will be a whole number, like 5% or 6%, or fractional, with some number of eighths included. However, there are some lenders that might use a marketing rate such as 4. 99% rather of 5% because it sounds a lot betterdoesn't it?Either method, when utilizing loan calculators make certain to input the proper rate to guarantee accuracy. There are a variety of factors, including the state of the economyRelated bond yields like the 10-year TreasuryAnd loan provider and investor hunger for MBSAlong with borrower/property-specific loan attributesAlthough there are a range of various aspects that affect rates of interest, the movement of the 10-year Treasury bond yield is said to be the very best indicator to figure out whether home mortgage rates will rise or fall. Treasuries are also backed by the "complete faith and credit" of the United States, making them the standard for numerous other bonds also. [Mortgage rates vs. house costs] Furthermore, 10-year Treasury bonds, also referred to as Intermediate Term Bonds, and long-lasting fixed home mortgages, which are packaged into mortgage-backed securities (MBS), contend for the same financiers due to the fact that they are relatively similar financial instruments. A simple way to think the instructions of home loan ratesIs to look at the yield on the 10-year TreasuryIf it goes up, expect mortgage rates to riseIf it decreases, anticipate home mortgage rates to dropTypically, when bond rates (also referred to as the bond yield) increase, rates of interest go up too. Do not puzzle this with, which have an inverted relationship with rate of interest. Financiers rely on bonds as a safe financial investment when the economic outlook is poor. When purchases of bonds increase, the associated yield falls, therefore do home loan rates. But when the economy is expected to do well, financiers leap into stocks, forcing bond costs lower and pressing the yield (and rate of interest) higher. An Unbiased View of What Is The Interest Rate On Mortgages

You can find it on financing sites alongside other stock tickers, or in the newspaper. If it's moving greater, home mortgage rates most likely are too. who has the best interest rates on mortgages. If it's dropping, http://angelolcds806.image-perth.org/the-only-guide-for-what-banks-give-mortgages-without-tax-returns mortgage rates might be improving as well. To get an idea of where 30-year repaired rates will be, utilize a spread of about 170 basis points, or 1. This spread represent the increased threat connected with a home loan vs. a bond. So a 10-yr bond yield of 4. 00% plus the 170 basis points would put mortgage rates around 5. 70%. Obviously, this spread can and will vary over time, and is actually just a fast way to ballpark home loan interest rates. So simply because the 10-year bond yield rises 20 basis points (0. 20%) does not suggest home mortgage rates will do the same. In reality, mortgage rates might rise 25 basis points, or just 10 bps, depending upon other market elements. Keep an eye on the economy too to determine directionIf things are humming along, mortgage rates might riseIf there's worry and misery, low rates might be the silver liningThis all relates to inflationMortgage interest rates are really susceptible to financial Website link activity, similar to treasuries and other bonds. unemployment] As a guideline of thumb, bad economic news brings with it lower mortgage rates, and good economic news forces rates higher. Keep in mind, if things aren't looking too hot, financiers will offer stocks and rely on bonds, which suggests lower yields and interest rates. If the stock exchange is increasing, home loan rates probably will be too, seeing that both climb on positive economic news. When they release "Fed Minutes" or alter the Federal Funds Rate, home mortgage rates can swing up or down depending on what their report indicates about the economy. Typically, a growing economy (inflation) causes higher home mortgage rates and a slowing economy causes lower home loan rates. Inflation also greatly impacts home loan rates. If loan originations escalate in a provided time period, the supply of mortgage-backed securities (MBS) might increase beyond the associated need, and rates will require to drop to end up being attractive to purchasers. This suggests the yield will rise, thus pushing home mortgage rate of interest higher. In brief, if MBS rates go up, home loan rates need to fall. An Unbiased View of What Is The Interest Rate On Reverse Mortgages

But if there is a purchaser with a healthy appetite, such as the Fed, who is scooping up all the mortgage-backed securities like insane, the rate will go up, and the yield will drop, hence pressing rates lower. This is why today's mortgage rates are so low. Just put, if loan providers can sell their home loans for more cash, they can offer a lower rates of interest. Considering that the value of the home is a crucial element in comprehending the risk of the loan, identifying the worth is a crucial consider mortgage lending. The value might be identified in numerous ways, however the most typical are: Actual or transaction worth: this is usually taken to be the purchase cost of the residential or commercial property. Assessed or surveyed value: in most jurisdictions, some form of appraisal of the value by a certified expert prevails. how much is mortgage tax in nyc for mortgages over 500000:oo. There is frequently a requirement for the lender to acquire an official appraisal. Estimated worth: lending institutions or other parties might use their own internal estimates, especially in jurisdictions where no authorities appraisal procedure exists, however likewise in some other circumstances. Typical procedures include payment to earnings (mortgage payments as a portion of gross or earnings); financial obligation to income (all debt payments, consisting of mortgage payments, as a percentage of earnings); and various net worth procedures. In many countries, credit rating are utilized in lieu of or to supplement these procedures. the specifics will vary from place to location. Earnings tax incentives generally can be used in types of tax refunds or tax deduction plans. The first suggests that income tax paid by individual taxpayers will be reimbursed to the extent of interest on home loan taken to acquire residential home. Some lenders might also require a prospective customer have several months of "reserve properties" offered. Simply put, the debtor may be needed to show the schedule of enough properties to spend for the real estate expenses (including home mortgage, taxes, and so on) for a duration of time in case of the job loss or other loss of income. Many nations have an idea of basic or conforming mortgages that timeshare review define a perceived appropriate level of risk, which might be official or casual, and might be reinforced by laws, federal government intervention, or market practice. For instance, a standard home mortgage might be thought about to be one with no more than 7080% LTV and no more than one-third of gross earnings going to mortgage financial obligation. The Only Guide to What Percentage Of Mortgages Are Below $700.00 Per Month In The United States

In the United States, an adhering home loan is one which meets the recognized rules and treatments of the 2 significant government-sponsored entities in the housing financing market (consisting of some legal requirements). In contrast, lenders who decide to make nonconforming loans are exercising a higher danger tolerance and do so knowing that they deal with more obstacle in reselling the loan. Controlled loan providers (such as banks) might undergo limitations or higher-risk weightings for non-standard home mortgages. For instance, banks and home loan brokerages in Canada deal with restrictions on providing more than 80% of the residential or commercial property worth; beyond this level, mortgage insurance is generally required. In some countries with currencies that tend to depreciate, foreign currency home mortgages are typical, enabling lenders to lend in a steady foreign currency, whilst Click here! the debtor handles the currency danger that the currency will depreciate and they will for that reason require to transform higher amounts of the domestic currency to repay the loan. Total Payment = Loan Principal + Costs (Taxes & charges) + Total interests. Repaired Interest Rates & Loan Term In addition to the 2 standard means of setting the expense of a mortgage loan (fixed at a set rates of interest for the term, or variable relative to market interest rates), there are variations in how that expense is paid, and how the loan itself is repaid. There are likewise various mortgage repayment structures to fit various kinds of borrower. The most common way to repay a secured mortgage loan is to make routine payments towards the principal and interest over a set term. [] This is frequently described as (self) in the U.S (what were the regulatory consequences of bundling mortgages). and as a in the UK. Particular information may specify to different areas: interest may be calculated on the basis of a 360-day year, for example; interest might be intensified daily, yearly, or semi-annually; prepayment penalties might use; and other elements. There may be legal restrictions on particular matters, and customer defense laws may specify or forbid particular practices.

In the UK and U.S., 25 to thirty years is the normal optimum term (although shorter periods, such as 15-year mortgage loans, are typical). Home loan payments, which are normally made monthly, include a payment of the principal and an interest aspect. The amount approaching the principal in each payment varies throughout the term of the home loan. Little Known Facts About What Is The Deficit In Mortgages.

Towards the end of the mortgage, payments are mostly for principal. In this way, the payment amount identified at outset is determined to guarantee the loan is repaid at a specified date in the future. This provides borrowers guarantee that by preserving repayment the loan will be cleared at a specified date if the rate of interest does not alter. Likewise, a mortgage can be ended prior to its scheduled end by paying some or all of the rest prematurely, called curtailment. An amortization schedule is normally exercised taking the primary left at the end of each month, increasing by the regular monthly rate and then deducting the month-to-month payment (percentage of applicants who are denied mortgages by income level and race). This is normally produced by an amortization calculator utilizing the following formula: A = P r (1 + r) n (1 + r) n 1 \ displaystyle A =P \ cdot \ frac r( 1+ r) n (1+ r) n -1 where: A \ displaystyle is the routine amortization payment P \ displaystyle P is the principal amount borrowed r \ displaystyle r is the rate of interest revealed as a portion; for a regular monthly payment, take the (Annual Rate)/ 12 n \ displaystyle n is the number of payments; for month-to-month payments over thirty years, 12 months x thirty years = 360 payments. This type of mortgage prevails in the UK, specifically when connected with a regular investment strategy. With this plan regular contributions are made to a separate investment plan designed to develop a swelling sum to pay back the home loan at maturity. This type of plan is called an investment-backed mortgage or is frequently related to the kind of plan used: endowment home loan if an endowment policy is used, likewise a individual equity plan (PEP) home mortgage, Person Cost Savings Account (ISA) home loan or pension home loan. Investment-backed mortgages are viewed as higher danger as they depend on the financial investment making sufficient return to clear the debt. Until recently [] it was not uncommon for interest only home mortgages to be organized without a payment vehicle, with the customer gambling that the residential or commercial property market will increase adequately for the loan to be paid back by trading down at retirement (or when rent on the residential or commercial property and inflation combine to exceed the rates of interest) []. The problem for lots of people has been the fact that no payment vehicle had actually been implemented, or the car itself (e. g. endowment/ISA policy) carried out poorly and therefore insufficient funds were readily available to repay balance at the end of the term. Moving forward, the FSA under the Home Loan Market Evaluation (MMR) have mentioned there should can i legally cancel my timeshare be strict criteria on the repayment car being used. The mortgage is in between the loan provider and the property owner. In order to own the home, the debtor agrees to a monthly payment over the payment period agreed upon. When the property owner pays the home mortgage in complete the lender will approve deed or ownership. Your month-to-month mortgage payment consists of a percentage of your loan principal, interest, real estate tax and insurance coverage. Many home mortgage loans last between 10, 15 or 30 years and are either fixed-rate or adjustable-rate. If you select a fixed-rate home loan, your rates of interest will stay the very same throughout your loan. But if your home loan is adjustable, your mortgage's rates of interest will depend upon the marketplace each year, meaning that your month-to-month payment could vary. If a homeowner does not make payments on their home mortgage, they might https://www.timesharestopper.com/blog/why-are-timeshares-a-bad-idea/ deal with late fees or other credit charges. The mortgage likewise gives the lending institution the right to take ownership of and offer the property to somebody else, and the house owner can face other charges from the lending institution. All in all, home loans are a great, affordable option for acquiring a home without the concern of paying in full upfront. The Single Strategy To Use For What Is Required Down Payment On Mortgages

Refinancing can be a clever option for house owners aiming to reduce their existing interest rate or month-to-month payments. It is vital for homeowners to comprehend the information of their primary mortgage in addition to the re-finance terms, plus any associated costs or fees, to make sure the choice makes monetary sense. In general, property buyers with good credit report of 740 or greater can expect lower rate of interest and more choices, including jumbo loans. Your rate will likewise be calculated based upon the loan-to-value ratio, which considers the portion of the home's value that you're paying through the loan. A loan-to-value ratio greater than 80% might be considered risky for lenders and result in greater rates of interest for the house purchaser. Nevertheless, bear in mind that these rates of interest are a typical based upon users with high credit history. Currently, an excellent rates of interest will be about 3% to 3. 5%, though these rates are traditionally low. The Federal Reserve impacts home mortgage rates by raising and lowering the federal funds rate. How What Is The Current Variable Rate For Mortgages can Save You Time, Stress, and Money.

As you go shopping for a loan provider, your genuine estate agent might have a few favored options, but all of it boils down to what works best for you. The Federal Trade Commission (FTC) advises getting quotes from different lenders and calling several times to get the very best rates. Be sure to ask about the interest rate (APR) and rates of interest. Some typical expenses may include appraisal and processing fees. Make sure to ask about any charges that are unknown and if they can be worked out. For the finest rates, you need to try to get preapproved by several lending institutions prior to deciding. Buying a home is a big step and your mortgage lending institution plays an important function at the same time. Most significantly, check out any documentation and the fine print so there aren't any unexpected charges or expectations. The Consumer Financial Defense Bureau has a loan quote explainer to assist you confirm all the details agreed upon between you and your lender. When requesting a home loan, the type of loan will normally identify how long you'll have your home loan. 3 Easy Facts About What Is The Current Index Rate For Mortgages Described

With a shorter term, you'll pay a higher regular monthly rate, though your overall interest will be lower than a 30-year loan. If you have a high month-to-month income as well as long-lasting stability for the foreseeable future, a 15-year loan would make sense to conserve cash in the long-lasting. However, a 30-year term would be better for somebody who needs to make lower regular monthly payments. By great rule of thumb, you should just be investing 25% to 30% of your regular monthly earnings on real estate every month. The Federal Housing Administration and Fannie Mae set loan limits for traditional loans. By law, all home loan have an optimum limit of 115% of typical house prices. Currently, the loan limitation for a single system within the United States is $510,400. Government-insured loans such as FHA have actually similar limits based on existing real estate rates. At the end of 2019, the FHA limitation was increased to $331,760 in the majority of parts of the country. VA loan limits were eliminated in early 2020. There's a big distinction between the interest rate (APR) and the interest rate. Facts About What Is A Min Number For Mortgages Uncovered

Here's the big difference your APR is a breakdown of whatever you're paying throughout the house purchasing procedure, including the rates of interest and any additional costs. APRs might also include closing expenses and other lender costs. APRs are usually higher than rate of interest because it's a breakdown of all fees you'll be paying, while the rate of interest is entirely the overall expense of the loan you'll pay.

It's the overall amount you're paying for obtaining the cash. On the other hand, the rate of interest is the rate, without costs, that you're being charged for the loan. The rate of interest is based upon aspects consisting of the loan quantity you consent to pay and your credit rating. Rate of interest can likewise vary depending upon the type of loan you choose and your state, in addition to some other aspects. What may not be readily apparent, though, is how fluctuations in your rate can make a significant impact. Let's take an appearance at what would happen if a 30-year fixed-rate home loan of $350,000 went up by just 0. 1%. Using a mortgage rate calculator, you can see your monthly home loan payment would increase from $1,773 to $1,794 if your rate increased from 4. The 10-Second Trick For What To Know About Mortgages In Canada

6%. That does not seem so bad, right?However, take a look at the overall interest you'll accumulate and pay during the life of the 30-year mortgage. That small 0. 1% increase in your rate is the difference in between $288,422 in interest payments and $295,929. And if your fixed-rate mortgage was an ARM instead, that space could be significantly greater 10s of thousands higher. Citizens BankOnline tools6203. 5% 13TD BankGovernment loans7003% 19Bank of AmericaDiscounts for existing customers6203% 5% * 50Quicken LoansFlexible terms5803. 5% 50New American FundingNo minimum payment6200% 48J. G. WentworthLow-income options5803% 45USAA MortgageCustomer service6200% 50SunTrust MortgageDiverse loan types6203% 50ChaseOnline home mortgage tracking6203% 40 The Coronavirus pandemic has actually caused considerable reductions to mortgage rates as demand plummeted. With Americans sequestered in their houses, the marketplace has stalled with no brand-new properties, no new sales, and no new buyers. Unemployment stays at an all-time high, but renewed commerce ought to produce brand-new purchasers and continue to increase need. As the weeks continue to pass, specialists forecast the marketplace will gradually start https://www.timesharestopper.com/blog/what-happens-if-i-just-stop-paying-my-timeshare/ to rebound, and we will see home loan rates rise in reaction as the country continues to recuperate. The 5-Second Trick For What Is A Hud Statement With Mortgages

Tips for Comparing Home Mortgage LendersEven if you choose to get quotes from numerous mortgage suppliers online, you can likewise examine local mortgage suppliers. Your local newspaper probably supplies quotes for some of the most competitive home loan lending institutions in your community. You might find that dealing with a regional home loan service provider is most convenient (what is the current index rate for mortgages). |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed