|

Like life insurance coverage, home mortgage security policies pay a benefit when the insurance policy holder dies, but the beneficiary is always the mortgage lending institution - not your family or some other recipient that you get to designate. It's useful to consider home loan protection as a restricted type of life insurance with more particular rules about who and how much is paid by the policy. Private home loan insurance (PMI) is a coverage that lenders need when your deposit is below 20 percent, and it safeguards the lending institution's cash in case you default. Many house owners are confused about the difference in between PMI (personal mortgage insurance) and home mortgage defense https://postheaven.net/arthus5ejk/this-lets-you-judge-the-lending-institutionand-39-s-service-and-make-sure-you insurance. The 2 are very differentand it is essential to comprehend the distinction in between them. It's not unusual for house owners to mistakenly believe that PMI will cover their mortgage payments if they lose their task, end up being disabled, or pass away. PMI is designed to secure the loan provider, not the homeowner. Home loan security insurance coverage, on the other hand, will cover your mortgage payments if you lose your job or become handicapped, or it will settle the home loan when you pass away. Read on to read more about the distinction between PMI and home mortgage security insurance coverage. PMI has absolutely nothing to do with task loss, special needs, or death and it will not pay your home mortgage if propel financial services llc one of these things occurs to you. If your deposit on your home is less than 20%, your lender will more than likely require you to get PMI. how many mortgages in one fannie mae. When you reach the point where the loan-to-value ratio is 80%, contact your home loan servicer (the business you make your payments to) and let it know that you wish to terminate the PMI premiums. An Unbiased View of How Much Is Mortgage Tax In Nyc For Mortgages Over 500000:oo

Even if you do not ask for a cancellation of PMI, the lending institution needs to immediately cancel it once the loan-to-value ratio gets to 78%. The expense of PMI varies, however is normally around one half of 1% of the loan quantity, so it is well worth the effort to eliminate it as quickly as you can, if you can. Home loan security insurance, unlike PMI, secures you as a borrower. This insurance generally covers your mortgage payment for a certain amount of time if you lose your job or end up being handicapped, or it pays it off when you pass away. Also unlike PMI, this kind of insurance is purely voluntary. If you remain in health, fairly secure in your task, have no uncommon lifestyle dangers, and are properly otherwise insuredfor example, you have life insuranceyou might not desire or require to acquire this type of insurance. For many of us, our home is our most significant financial investment in addition to our family haven. Losing a breadwinner can wreak havoc on the family's finances and their ability to remain in the home they enjoy. So, what's the very best way to protect your house in case something happens to you? Here are 2 alternatives: home mortgage security insurance and conventional term life insurance coverage. Home mortgage defense insurance coverage (MPI) is a type of life insurance coverage created to pay off your home loan if you were to die and some policies likewise cover mortgage payments (typically for a limited duration of time) if you become handicapped. Note: Don't confuse MPI with personal mortgage insurance (PMI), which protects the lender if you default on the loan. Guaranteed approval. Even if you remain in poor health or operate in an unsafe occupation, there is ensured approval without any medical tests or lab tests. No uncertainty. The check goes straight to the lending institution for the specific home mortgage balance, so there'll always be enough and your family will not need to deal with the cash.

Excitement About Reddit How Long Do Most Mortgages Go For

Some MPI policies make home loan payments (usually for a limited time) if you end up being handicapped or lose your task. Absence of flexibility. MPI offers recipients no option. The insurance coverage settles the home loan nothing else. This implies your family can't utilize the money for anything else. Higher cost. MPI typically costs more than term life insurance coverage, specifically for healthy, accountable grownups. Diminishing protection. As your home mortgage balance declines, the policy's payout decreases with it. That suggests you'll end up paying the very same cost for less coverage with time. More restrictive age limits. MPI policies often have more limiting concern ages than term life. For example, some insurers won't release a 30-year MPI policy to anyone over age 45. Let's take a more detailed look. Term life is developed to pay an advantage to the person( s) or organization( s) you designate if death occurs during a specific amount of time. You choose the advantage quantity and the time period. The rate and benefit quantity generally remain the same for the entire term. Your family can decide how to utilize the earnings. They can utilize it to settle the home mortgage or for something else like replacing lost earnings, investing it for retirement, paying tuition or covering pressing costs like burial expenditures. Lower expense. Term life can be very budget-friendly and most likely costs less than you believe. Coverage never ever decreases. The protection amount you select when you use will remain the exact same throughout the whole regard to protection. Cost never increases. With conventional term, the rate is ensured to stay the same for the length of the coverage period. The expense for many MPI policies can change later on. How To Rate Shop For Mortgages Fundamentals Explained

Term life is normally offered at greater ages than MPI. For example, Grange Life problems 30-year term policies approximately age 55 that last to age 85. Additional defense. Some term policies provide "living advantages" in addition to a survivor benefit, allowing you to access the survivor benefit early under particular circumstances (like terminal health problem). Many people can get approved for coverage though the rate might be greater for those with health, driving or monetary issues. Coverage isn't coordinated with your home mortgage. So, you require to make certain you select enough coverage to cover the balance of your home mortgage. Your household will be responsible for sending out the payment to the lending institution. With MPI, there will never be additional money going to your household. If you own your house complimentary and clear, MPI could timeshare maintenance fee increases be a waste of cash. And the majority of people don't require MPI if they have sufficient life insurance coverage (even if those solicitations state otherwise). If you do not have adequate life insurance coverage, think about getting more. Nevertheless, for those who have difficulty getting traditional life insurance, MPI can offer important security that may not otherwise be offered to you and the extra cost may be worth it. Before you choose, get estimate and contact your local independent insurance representative to see if you 'd get approved for term life insurance coverage. Do not have a representative? You can discover a Grange Life agent near you. This short article is not intended to be utilized, nor can it be used, by any taxpayer for the purpose of avoiding U.S. federal, state or local tax charges. It is written to support the promotion of the matter addressed here. The Best Strategy To Use For Where To Get Copies Of Mortgages East Baton Rouge

Any taxpayer must consult based on his/her particular scenarios from an independent tax consultant. All life policies are financed by Grange Life Insurance Coverage Business, Columbus OH, or Kansas City Life, Kansas City, MO, and go through underwriting approval. Not readily available in all states. Referrals:- LIMRA.

0 Comments

A reverse mortgage works by permitting house owners age 62 and older to obtain from their home's equity without needing to make month-to-month mortgage payments. As the customer, you might choose to take funds in a lump amount, credit line or through structured month-to-month payments. The repayment of the loan is needed when the last enduring debtor vacates the home permanently. The traditional loan is a falling debt, rising equity loan, while the reverse mortgage is a falling equity, rising financial obligation loan. Simply put, as you pay on a conventional loan, the amount you owe is reduced and therefore the equity you have in the property increases in time. There is a secret here that I am going to let you in on - how many mortgages are there in the us. There is never a payment due on a reverse home loan and there is also no prepayment penalty of any kind. Simply put, you can make a payment at any time, approximately and consisting of payment completely, without penalty. The amount of cash you can get from a reverse mortgage normally varies from 40-60% of your house's assessed value. The older you are, the more you can receive as loan quantities are based mostly on your life span and existing interest rates - which credit report is used for mortgages. The age of the youngest customer Value of the home or the HUD lending limit (whichever is less) The rate of interest in impact at the time Costs to acquire the loan (which are deducted from the Principal Limit) Existing mortgages and liens (which should be paid completely) Any staying money comes from you or your successors. The Principal Limitation of the loan is identified based upon the age of the youngest customer due to the fact that the program utilizes actuarial tables to determine the length of time customers are most likely to continue to accumulate interest. If there are several borrowers, the age of the youngest borrower will lower the amount offered since the terms permit all debtors to live in the home for the rest of their lives without needing to make a payment - how does chapter 13 work with mortgages.

Rumored Buzz on How Is Lending Tree For Mortgages

There are several methods debtors can get funds from a reverse home mortgage: A cash swelling amount at closing A line of credit that you can draw from as required A payment for a set quantity and duration, called a "term payment" A guaranteed payment for life (called a "tenure payment") which lasts as long as you reside in your home. For instance, a couple born Browse around this site in 1951 that owns outright a $500,000 home may choose it is time to get a reverse home loan. They would like $100,000 at closing to make some improvements to their residential or commercial property and fund a college strategy for their grandchild. how did subprime mortgages contributed to the financial crisis. They have a bigger social security advantage that will begin in 4 years, but up until then, wish to augment their earnings by $1,000 monthly - what does ltv stand for in mortgages. That would leave an additional $125,000 in a Learn more here line of credit that would be available to use as they require. In addition, they would receive a guaranteed development rate on their unused line of credit funds. In the past, many considered the reverse home loan a last option. Let us think about a borrower who is savvy and is planning for her future needs. So, she obtains her reverse mortgage and after the costs to acquire the loan has the same $200,000 line of credit available to her. Her credit line grows at the exact same rate on the unused portion of the line as what would have accrued in interest and had she borrowed the cash. If rates do not alter, here is what her access to credit appears like in time: Remember, that is just if rates do not alter. If interest rates go up 1% in the third year and one more https://truxgo.net/blogs/68989/74600/our-how-do-mortgages-payments-work-diaries percent in the 7th, after 20 years her available credit line would be more than $820,000. The Buzz on How Many Types Of Reverse Mortgages Are There

You or your heirs would have to pay it back when the residential or commercial property sells. But where else can you make sure that you will have in between $660,000 and $800,000 readily available to you in 20 years? The calculator is revealed listed below, and you can see the really modest rate increases used. If the accrual rates increase more the development rate will be greater. Suggesting you must take the full draw of all the cash readily available to you at the close of the loan. You can not leave any funds in the loan for future draws as there are no future draws enabled with the fixed rate. Since customers experienced a much greater default rate on taxes and insurance coverage when 100% of the funds were taken at the initial draw, HUD changed the method by which the funds would be readily available to customers which no longer allows all borrowers access to 100% of the Principal Limitation at the close of the loan. Reverse mortgage primary limitation aspects are based upon actuarial tables. Usually a 62-year-old will receive approximately 50% of the houses evaluated worth, where an 80-year-old will receive closer to 70%. Reverse home mortgages are not naturally excellent nor bad. The choice to take a reverse home mortgage needs to always be looked at as a specific technique weighing long-term suitability. Reverse mortgages do not come without expense. It is a loan against your house, and it does accumulate interest unless you decide not to make voluntarily repayments. The longer you keep a reverse home loan balance, the greater the interest charges end up being as interest itself substances over the life of the loan. The reverse home loan balance can be repaid at any time without penalty. You can pick to either pay back the loan willingly or defer interest up until you later on sell your house. When the loan balance will be paid in full any remaining equity will come from your successors or estate. Yes. The Definitive Guide to What Is The Debt To Income Ratio For Conventional Mortgages

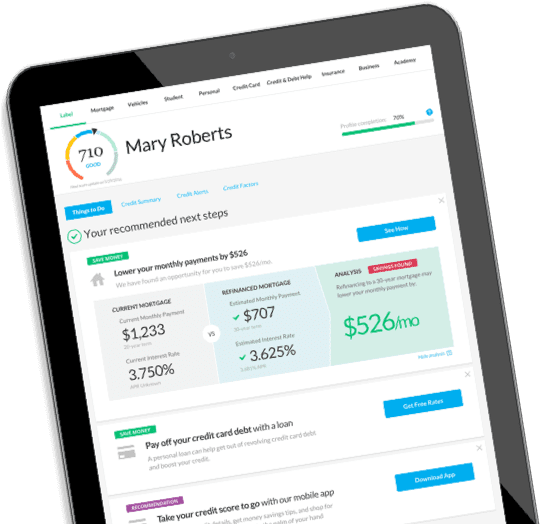

( Defined by not leaving longer than a 6-month duration). Need to you fail to keep the loan arrangement the servicer is required by HUD to call the loan due and payable. When it comes to rates, are more willing now than ever to help pay costs whenever they can on reverse home loans. If there is an existing home mortgage balance to benefit, there is frequently room in the value of the loan for the lending institution to make back cash they invest in your behalf when they offer the loan. Education is the key, while knowing your objectives will help you obtain a loan that is finest for you. An extremely will accumulate the least amount of interest when you start using the line, but if you are looking for the greatest amount of line of credit development, a greater margin grows at a greater rate. Understanding what you want out of your reverse home loan will assist you select the very best option that will get you there. As I specified earlier, we do not recommend reverse mortgages for everyone. If the loan does not satisfy your requirements and you are still going to be scraping to get by, you will require to face that fact prior to you start to utilize your equity. Based on the numbers you offered, here is your home mortgage estimate. Desire to see other choices? Just get in new numbers to compute and compare. Our company believe that outstanding service and a track record for sincerity, stability and reliability are simply as important as helping you discover the house of your dreams. We're https://blogfreely.net/annilar0rq/because-financial-regulation-and-institutional-reforms-make-a-return-of experiencing high telephone call volumes and appreciate your perseverance. Lots of queries can be resolved through our automated action system online. If you are requesting COVID-19 payment help, please email us at. Mr. Cooper is here to walk along with you in your homeownership journey in Brea, CA. As the third-largest home loan servicer and a top-20 house lending institution in the nation, we have the background to help you evaluate your loan choices and strengthen your house buying strategy. A Mr. Cooper home mortgage professional can create a custom strategy that will assist you deal with the home mortgage procedure with self-confidence. Our home mortgage experts will examine your unique monetary and living situation and will create an advised plan for the very best home loan alternatives that fit your needs. Discover more about different home mortgages below and get in touch with Mr. Cooper in Brea to take the primary step toward reaching your objective. Some Known Details About When Does Bay County Property Appraiser Mortgages

About 1 in 5 of all homebuyers go with this kind of government-insured loan. The loan system is specifically geared towards property buyers who can't afford the common 20% deposit that's normally required by private lending institutions. The down payment can be as low as 3. 5% and may be a perfect suitable for purchasers who can't get a standard loan. Cooper has actually viewed FHA loans rise in appeal along with increases in student loan debt and rental expenses two situations that can make it hard to put away cash for a down payment. Another perk to FHA loans is that they're typically offered to borrowers with lower credit history. Wherever you are on your journey, Mr. There's no concern about it. America's service members, veterans, and their partners should receive the very best. Mr. Cooper can provide their proficiency in assisting you get qualified for a VA house loan in Brea if you think you might be qualified for one. Get In Touch With Mr. when did subprime mortgages start in 2005. Cooper if you're seeking to purchase a home in Brea and want to learn more about VA loans. VA loans use lower rates when compared to the total mortgage landscape. There's also a possibility that you will not have to put down a deposit. Confirming your VA eligibility for a VA loan in Brea is quick and simple with a Mr. Cooper expert walking you through the application process. A jumbo home mortgage, or a jumbo loan, goes beyond the limits of a traditional loan. Jumbo loans are created to assist individuals refinance or purchase higher-valued realty and are frequently countless timeshare professionals dollars. If you want Browse around this site to utilize a jumbo loan to purchase a house in Brea, you will probably need a bigger loan quantity that goes beyond conventional loan limits. What Does Recast Mean For Mortgages Fundamentals Explained

Cooper for more details on jumbo loan eligibility in Brea. Mr. Cooper's team of home mortgage experts is ready to assist you through your house buying journey in Brea (when does bay county property appraiser mortgages). However we understand that does not suggest the same thing to everybody. Some people simply desire to inspect home loan rates in Brea. Others want to get preapproved for a home mortgage in Brea. Sort by: importance - date Page 1 of 2,047 jobs Shown here are Task Ads that match your query. Undoubtedly may be compensated by these companies, assisting keep Certainly free for jobseekers. Undoubtedly ranks Job Ads based on a mix of company bids and importance, such as your search terms and other activity on Indeed. Can package loan documents effectively for funding. From $20,000 a month You will take the NMLS test and start getting accredited in the states Proven Home mortgage operates and begin building your pipeline. Santa Ana, CA 92705 Briefly remote $18 - $32 an hour Quickly applyUrgently employing Verify and examine loan paperwork consisting of earnings, credit, appraisal, and title, while preserving stringent compliance with all suitable federal and state From $250,000 a year Contact pre-qualified customers to assist in a warm call transfer to a licensed Mortgage Loan Originator/Banker. From $16 an hour In addition, this position offers a basic rate salary with the eligibility of commission for each effectively moneyed loan! Costa Mesa, CA 92626 Remote Run MERS for fraud audit. Helping funders with jobs as required. High School diploma or equivalent. 1= years' mortgage experience in a similar function. Tested experience working with CRM software application. True Home Loan Irvine, CA 92618 Momentarily remote $120,000 - $500,000 a year Quickly applyUrgently employing We offer all of our loan officers direct to customer marketing with incoming calls, a generous indication on warranty, and a comp strategy ranging from 30 -100 basis Quickly applyUrgently hiring A great job for somebody simply going into the workforce or going back to the workforce with restricted experience and education. How Many Mortgages To Apply For Things To Know Before You Buy

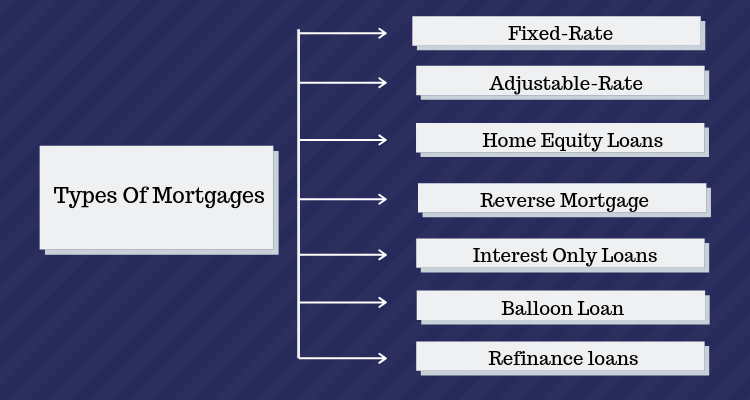

$ 15 - $18 an hour Quickly applyUrgently working with _ We will train the very best of the best in this department to end up being licensed Loan Officers. Multi-task efficiently by speaking and getting in client data. Delegate Funding Irvine, CA 92602 (Lower Peters Canyon location) From $14 an hour Become a licensed home mortgage lender in less than 6 months. $ 55,000 - $60,000 a year Quickly applyUrgently employing Knowledgeable about regulatory requirements relating to disclosures and mortgage files. Perform file reviews while adhering to regulative compliance and time Work with Department Supervisor and Loan Officers on regional marketing campaigns using Home loan Returns, Eaglehm. com leads, and so on. Communicate well with co-workers. Monday Friday 9 a. m. 5 p. m. Saturday 9 a. m.-1 p. m. 2500 E. Imperial Hwy. Suite 170Brea, CA 92821 Serving CU SoCal Members and CO-OP shared branch Members in Brea on the corner of Imperial Highway and Kraemer Boulevard. For check and money deposits, and cash withdrawals, there is likewise a CU SoCal ATM offered with 24-hour gain access to. Vacation Date Observed New Year's Day Friday, January 1 Martin Luther King Day Monday, January 18 President's Day Monday, February 17 Memorial Day Monday, Might 25 Self-reliance Day Friday, July 3, and Saturday, July 4 Labor Day Monday, September 7 Veteran's Day (Observed) Wednesday, November 11 Thanksgiving Thursday, November 26 Thanksgiving (Continued) Friday, November 27 Christmas Eve (open up until 1 p. Repaired rate mortgages are mortgages where the rates of interest stays the same for the entire term of the loan. The benefit to a set rate home mortgage is that if you lock a fairly low rate, your payment won't go up when rates do. With an adjustable rate home mortgage, the rate of the loan can alter throughout the regard to the loan. What Does Hud Have To With Reverse Mortgages? Can Be Fun For Anyone

A hybrid loan combines a set duration together with an adjustable part. Usually these loans are fixed for a time period and after that the loan ends up being adjustable where it depends on present rates. An FHA loan is a loan in the United States that is guaranteed by the Federal Real Estate Administration. The loan may be provided by qualified lending institutions. The VA was developed to provide long-term financing to American Veterans or to their enduring partners. It is not to your advantage to postpone informing your servicer [deadlines tend to be] based upon the date that the customer died not the date that the loan servicer was warned of the borrower's death." Do not be alarmed if you get a Due and Payable notice after informing the loan servicer of the debtor's death.

The loan servicer will offer you as much as 6 months to either settle the reverse home loan debt, by offering the home or utilizing other funds, or acquire the home for 95% of its current appraised value. You can request up to 2 90-day extensions if you require more time, but you will need to demonstrate that you are actively working towards a resolution and HUD will need to approve your demand. Whether you wish to keep the home, offer it to settle the reverse home loan balance, or ignore the property and let the lender deal with the sale, it is very important to keep in contact with the loan servicer. If, like Everson, you have difficulty handling the loan provider, you can send a grievance with the Consumer Financial Security Bureau online or by calling (855) 411-CFPB. " When the last house owner dies, HUD begins proceedings to take back the home. This results in a lot more foreclosure proceedings than actual foreclosures," he said. If you are facing reverse home loan foreclosure, deal with your loan servicer to deal with the scenario. The servicer can link you to a reverse mortgage foreclosure prevention therapist, who can deal with you to set up a repayment plan. We get contact a regular basis from people who believed they were entirely safe and secure in their Reverse Home mortgage (likewise called a "Home Equity Conversion Mortgage") however have now found out they are being foreclosed on. How is this possible if the business who owns the Reverse Home loan has made this contract with the property owner so they can live out their days in the home? The simple answer is to seek to your arrangement. 202 specifies a Home Equity Conversion Mortgage as "a reverse mortgage made to an elderly house owner, which home mortgage loan is protected by a lien on real estate." It also specifies an "senior property owner" as how much do timeshares cost per year someone who is 70 years of age or older. If the house is collectively owned, then both property owners are deemed to be "elderly" if at least among the property owners is 70 years of age or older. Fascination About What Is The Maximum Number Of Mortgages

If these clauses are not followed to the letter, then the mortgage company will foreclose on the home and you may be liable for particular costs. Some of these could include, however are not restricted to, default on paying Residential or commercial property Taxes or House owner's Insurance, Death of the Customer, or Failure to make prompt Repair work of the Residential or commercial property. In some cases it is the Reverse Mortgage lending institution that is expected to make the Real estate tax or pay the Homeowner's Insurance coverage similar to a traditional home loan might have these put into escrow to be paid by the loan provider. However, it is really typical that the Reverse Home loan homeowner need to pay these. The lending institution will do this to safeguard its financial investment in the home. If this holds true, then the most common option is to make certain these payments are made, offer the receipt of these payments to the lending institution and you will more than likely need to pay their lawyer's costs. Lots of Reverse Home loan clauses will state that they can speed up the financial obligation if a debtor dies and the home is not the principal home of a minimum of one enduring borrower. In the case of Nationstar Home mortgage Business v. Levine from Florida's 4th District Court of Appeal in 2017 the owner and his partner both resided in the property, however Mr. His partner was not on the mortgage and considering that Mr. Levine passed away, Nationstar exercised its right to speed up the debt and eventually foreclosed. Among the important things that can be performed in this case is for the partner or another household member to buy out the reverse mortgage for 95% of the assessed value of the home or the real expense of the financial obligation (whichever is less). The household can purchase out the loan if they wish to keep the home in the household. Another circumstances would be that ellen mcdowell if the home is damaged by some sort of natural disaster or from something else like a pipe breaking behind a wall. A number of these type of issues can be managed rather rapidly by the homeowner's insurance coverage. What Does What Are All The Different Types Of Mortgages Virginia Do?

If it is not repaired rapidly, the Reverse Mortgage loan provider might foreclose on the home. Just like the payment of the taxes and insurance, the way to handle this situation is to immediately look after the damage. This may indicate going to the insurer to make certain repairs get done, or to pay out of pocket to make certain they get done. In all of these instances, it is necessary to have a top-notch foreclosure defense group representing you for the duration of your case. You don't have to go this alone. If you or a member of the family is being foreclosed on from your Reverse Home mortgage, please offer the Haynes Law Group, P.A. We deal with foreclosure defense cases all over the state of Florida and will be able to give you assistance on what to do while representing you or your relative on the Reverse Home loan Foreclosure case. mortgages what will that house cost. The consultation is always complimentary. A reverse mortgage is a kind of home loan that is usually available to llc cancellation property owners 60 years of age or older that permits you to transform some of the equity in your home into cash while you keep ownership. This can be an attractive choice for senior residents who may discover themselves "house rich" but "money bad," but it is wrong for everyone. In a reverse home mortgage, you are obtaining cash versus the amount of equity in your house. Equity is the distinction between the appraised worth of your home and your impressive mortgage balance. The equity in your house increases as the size of your mortgage shrinks and/or your residential or commercial property value grows. This suggests that you are paying interest on both the principal and the interest which has actually already accumulated monthly. Intensified interest triggers the impressive amount of your loan to grow at a significantly quicker rate - what metal is used to pay off mortgages during a reset. This means that a big part of the equity in your house will be utilized to pay the interest on the amount that the lending institution pays to you the longer your loan is impressive. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2022

Categories |

RSS Feed

RSS Feed